A Controller Oversight Service

You can see your loans. Can you see your loan book?

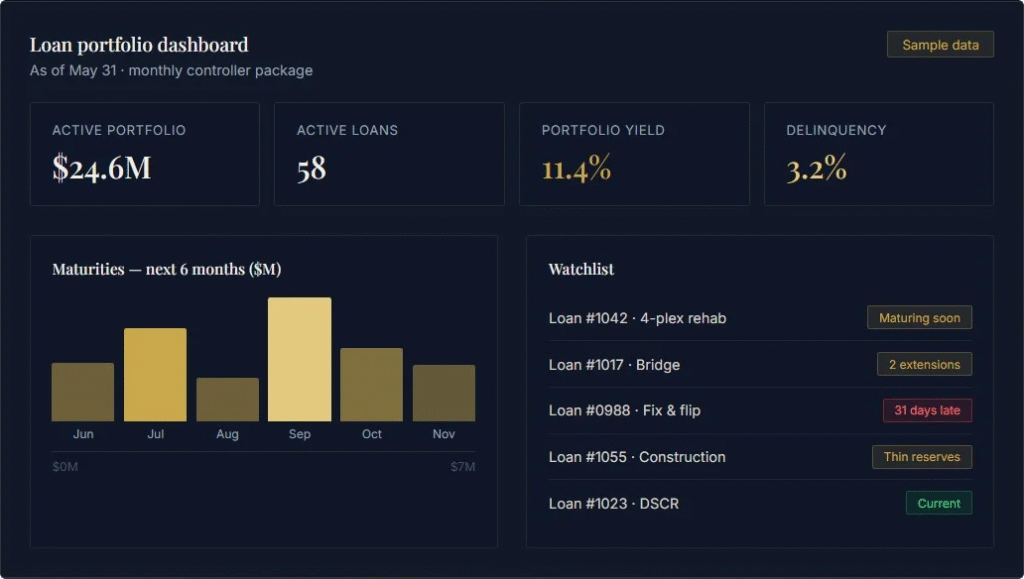

For a lender or debt fund, the portfolio is the business — and most leaders can see activity without seeing the financial truth underneath: yield by loan, which loans are profitable, where extensions are piling up, how delinquency is trending. The Financial Anchor gives leadership a clear financial view of the whole book, and flags the loans that need attention before they become problems.

What Most Lenders Can't See

You can’t see yield by loan.

Maturities arrive without warning.

Extensions pile up, and no one’s tracking the exposure.

Late and default activity is hard to see as a trend.

Fee income isn’t tied back to each loan.

You’re not sure the reserves match the risk.

What We Monitor

The most expensive loan problems are the ones nobody flagged in time.

We maintain a watchlist that surfaces loans worth a closer look — approaching maturity, repeated extensions, slipping into delinquency, thin reserves — so leadership can act early, while there are still options. Seeing a problem at 30 days is a decision. Seeing it at 120 is a loss.

See the whole book — and the loans that need you first.

☎ 281-972-4712